Treating Customers Fairly (TCF) is a regulatory requirement of the Financial Conduct Authority that encourages firms to put customers at the heart of their business model. A company that treats customers fairly according to the FCA’s Handbook means that applicants will have clear access to information about the products that they are applying for (benefits, costs, risks) and minimise the sale of a product that is not suitable for them either before, during or after its sale. (Source: TCFinfo)

![]()

This concept applies to lenders, sole traders and comparison websites too. At Guarantor Loan Comparison, we review every lender before featuring them on our website to ensure that they have authorisation with the FCA and have a culture dedicated to Treating Customers Fairly. So when you are looking for loans with a guarantor, you can be rest assured that your details will be held securely, the information will be transparent and you will not be offered loans that are unsuitable.

Treating Customers Fairly Consumer Outcomes

The notion of TCF notoriously has 6 outcomes that will benefit the consumer:

(Source: FCA.org.uk)

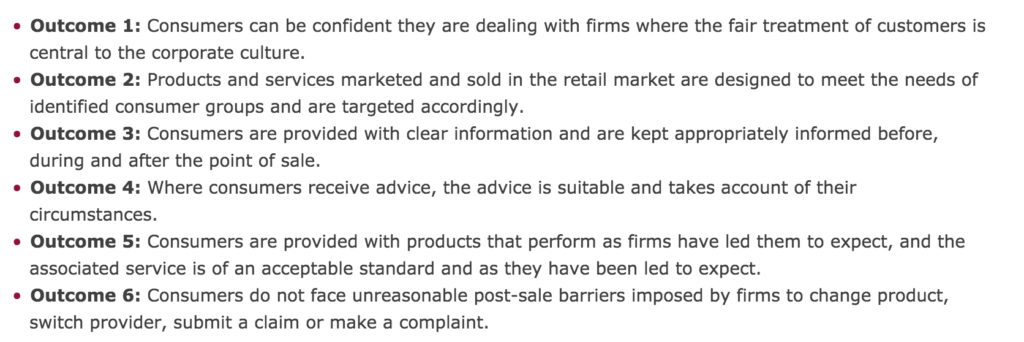

Outcome 1: Consumers can be confident they are dealing with firms where the fair treatment of customers is central to the corporate culture.

This means that lenders, brokers and advisors will not only offer TCF on the odd occasion or for certain aspects of their business. Instead, putting customers first it is a fundamental thing that they do from the beginning and is manifest in every part of their business such as advertising, website, customer service, underwriting, collections and more.

Outcome 2: Products and services marketed and sold in the retail market are designed to meet the needs of identified consumer groups and are targeted accordingly.

Customers should not be sold products that are inappropriate for them, such as being unnecessary, impractical or would cause financial difficulty. An example is offering a maximum loan amount to someone with a low income or giving someone finance if they are on benefits or unemployed. A key feature of this is carrying out sufficient credit and affordability checks to get a better idea of the applicant’s circumstances and then match them with the appropriate product.

Outcome 3: Consumers are provided with clear information and are kept appropriately informed before, during and after the point of sale.

Borrowers should be able to see very clearly how much they are borrowing, the cost of it and when they are required to repay and how much. This information can be accessible on the website and also in the terms of the loan agreement and contract. Lenders and brokers must not try to hide anything in the small print and the customer should have a clear understanding of what to expect from their loan.

Outcome 4: Where consumers receive advice, the advice is suitable and takes account of their circumstances.

An individual must be given impartial advice and relative to their financial circumstances. This is an area where some companies have attracted criticism in the past. To give an example, whilst it might be more profitable for the company to keep re-financing a customer’s loan, a company that treats customers fairly will know that this is not best for them long-term, so may recommend some alternative credit or debt management services.

Outcome 5: Consumers are provided with products that perform as firms have led them to expect, and the associated service is of an acceptable standard and as they have been led to expect.

This means that the lender has to deliver what they have promised. If they say that they will fund within 24 hours and will offer the interest rate presented in the loan agreement, they have to keep to this.

Outcome 6: Consumers do not face unreasonable post-sale barriers imposed by firms to change product, switch provider, submit a claim or make a complaint.

If the customer wants to make a complaint, cancel the loan or switch providers, they must be able to do so. All the guarantor lenders we work with all you to repay your loan early if you wish to and you may find that if you have the funds to clear your account, you will make a big saving by repaying early. The only area that might be tough is if your guarantor no longer wants to be involved or dies, in which case they may require an alternative or next of kin to take over.

(Source: MoneyAware.co.uk)

Customer Feedback For Treating Customers Fairly

To ensure that companies are truly doing what is best for the customer, there needs to be a way for borrowers to give their feedback before, during or after the sale of a product. Whether this is through a complaints policy on their website, contact email address or review sites like TrustPilot and Reviews.co.uk – customers need to be able to give their views on how they have been treated, positive or negative.

What TCF is not

It is important to find the balance between satisfied customers and treating them fairly. Don’t forget that just because a customer is satisfied, does not mean that they were necessarily treated fairly – as they could have been allowed to borrow more despite putting a strain on their finances. So being able to offer feedback during or after the sale of the loan is key.

Not all firms need to be identical in their practices. The FCA accepts that some firms in the same industry offer variations of their products and have different technical abilities when it comes to underwriting and affordability checks.

The FCA does not have a final say on every single product that is sold. The lenders and brokers have a responsibility to find the right product for the customer. The APR is always expressed as a representative so that it is the rate offered to at least 51% of customers.

Where TCF can be implemented

Treating Customers Fairly is an essential part of the corporate culture and therefore must be present in every aspect of the organisation including:

- Advertising and Marketing (website, promotions, adverts)

- Staff culture (training and awareness)

- Product design (fees, loan amounts, loan terms)

- Underwriting (checks carried out)

- Sales process (lead generation)

- Customers service (answering questions and collections)

- Advice (helpful and impartial)

- Complaint handling (allow for customer feedback)

- Record keeping and management information

In conclusion, TCF is a very important part of providing compliant loan services in the UK. By companies making TCF a key part of their corporate identity and culture, it allows for better practices across the entire industry, which ultimately leads to an increase in consumer confidence and better business for everyone involved. Therefore, those lenders, brokers, advisors and comparison websites that follow TCF the best, will reap the greatest rewards.