Bank Unauthorised Overdrafts More Expensive Than Payday Loans

Payday loans are commonly criticised in the press for being too expensive, and their sister guarantor loans also don’t get off easy. Before the FCA regulation come into effect in January 2015, the payday industry charged representative APRs of 1,000% up to 6,000% – which led to a lot of backlash from MPs, journalists and religious figures.

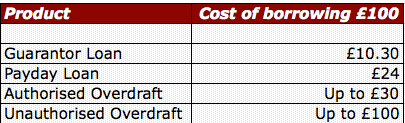

However, in reality, those loans of up to £1,000 that are supposed to last you until payday are actually on par with your bank overdraft fees and are significantly cheaper than your unauthorised overdraft that you get from current accounts and credit cards.

The new FCA rules have capped the amount a payday lender can charge to 0.8% per day or £124 per £100 borrowed.

Overdraft vs Loan Comparison

The guarantor loan is based on an example from Amigo loans for £500 repaid over 12 months at £51.53 per month.

When you receive a current account or credit card from bank or provider, you will likely have access to an overdraft. Whilst the creditor gives you a ‘credit limit’ each month, this is the maximum you can use on your credit limit without extra charges and is based on your affordability and credit score. So typically if you repay your credit card bills on time for a long period, they will increase your credit limit – so you can borrow more.

Your authorised overdraft is the amount you are allowed to go over the credit limit. So if your credit limit is £4,000, you may have an authorised overdraft of £1,000 which has been agreed between you and your credit provider and you can go over £1,000 each month, with some extra charges.

However, if you don’t know have authorised overdraft agreed beforehand, this will cause you to have an ‘unauthorised overdraft’ so if you want to go beyond your credit limit, you will pay huge fees as a result. For more information, read the guide on overdrafts from The MoneyAdviceService.

Based on our table above, the potential fees for going into your unauthorised overdraft are huge in comparison to a payday, guarantor loan or authorised overdraft.

How much is an authorised overdraft?

Your authorised overdraft is agreed with your bank or credit provider upon application and is based on:

- Your credit score (debt history)

- Your affordability i.e salary, expenses

- The provider’s terms and conditions

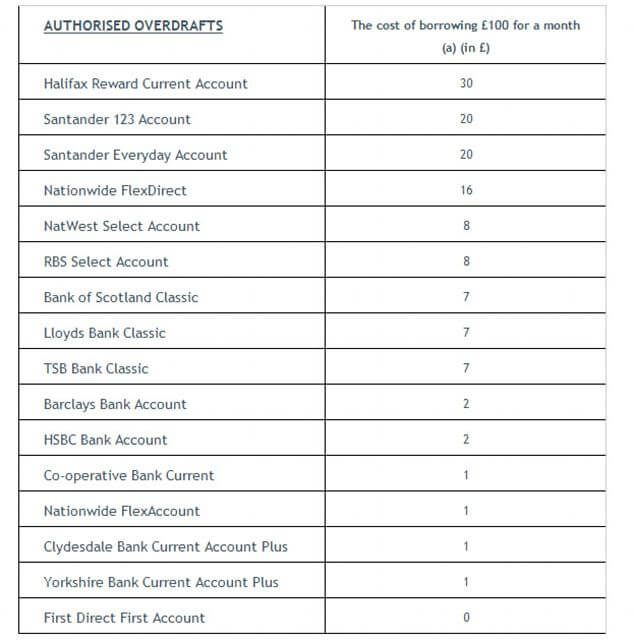

The rates vary between lenders with First Direct not charging anything for authorised overdrafts but Halifax charging as much as £30 per £100 borrowed. Even Santander’s account are considered quite high and on par with some payday lenders. (Source: This is Money)

How much is an unauthorised overdraft?

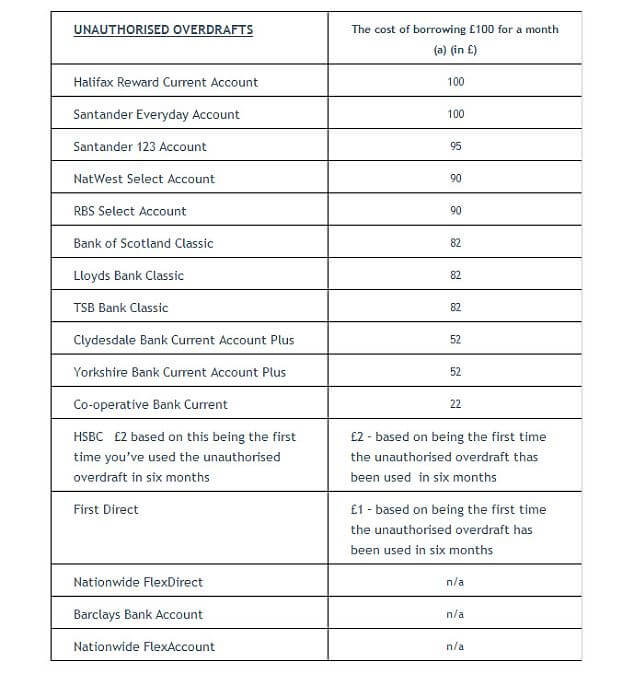

Unauthorised overdrafts are significantly more expensive because it is like borrowing without permission and means that the credit card company or credit account provider is taking on a lot of risk. Hence, the likes of Halifax and Santander charge up to £100 per £100 borrowed for using your overdraft facility. Other banks are not far behind with NatWest and RBS both charging £90 per £100 borrowed.

All of these should be used for emergencies only

The types of loan facilities mentioned about are ideal for emergency situations. They are more expensive than your standard personal loan and this is because they can accommodate those with bad credit and the funds can be made available instantly (with credit cards) and within 24 hours (payday and guarantor products).

To use these types of borrowing as a long term solution is not advisable and can lead to debt problems. They should not be used for funding lavish lifestyles or material things such as presents, holidays, new cars, jewellery or other consumer goods – they are better suited for emergencies like boiler problems, flooding in your home or medical bills as you will need money quickly and may not have any other option.

The best way to avoid these kind of fees is to save money for a rainy day or have a fund especially for emergencies. Some say it is best to have 3 months worth of your salary stashed away in case you need it. If you have to borrow money, consider using a credit union which is a not-for-profit organisation offers super low interest rates and no late fees for those working in the public sector or in the local neighbourhood.

Our website was set up to help you find the best loan for you. Our comparison table lets you compare guarantor loans so you can find the best one for your needs – based on loan amount, duration and representative APR. Our site is filled with advice and guides related to the application process and you have all the necessary information before applying.