Understanding Direct Debits and Standing Orders

Direct debits and standing orders are two of the most common ways to make regular and recurring payments to other individuals or companies. In this guide we explain how they both work, when you would use them and how they are different to each other. Plus, we explain how they are relevant for guarantor loans products.

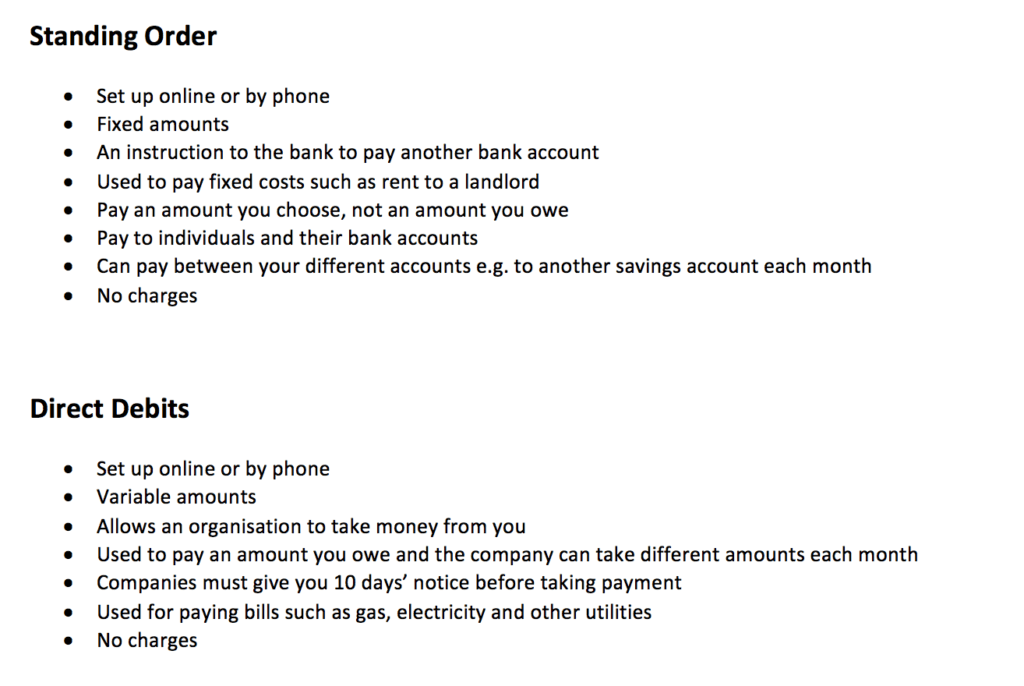

Overview

What is a Direct Debit?

Direct debits are probably the most common type of way to make regular repayments. Despite the name, you can set up a direct debit on both a debit card or credit card, depending on what you are paying for.

![]()

A direct debit is used to set up payments to another organisation that you are dealing with or are a customer of. Rather than having to call up and login every week or month to make a repayment, you can set up a automatic repayment through your bank either by phone, in branch or online (most popular). This is why direct debits are so convenient and used by millions of people.

Typical uses of a direct debit include:

- Paying your mobile phone bill

- Paying gas and electricity bills (variable amounts)

- Subscriptions such as Sky, Netflix or your local gym

By setting this up, you allow the organisation to take payments from your debit or credit card upon a scheduled date. You must give the bank or building society permission to do this. As per the regulatory requirements, the company must give you notice on the days leading up to the money being taken out of your account.

A key point about direct debits is that they pay variable amounts, meaning repayments can vary from month to month. A perfect example of this is your phone bill which will vary each month depending on your usage. You would not be able to use a standing order for this, which we explain below.

Using a direct debit as a method of payment is completely free. There are no additional bank or transaction charges incurred. In fact, some vendors and organisations will give you a discount for using a direct debit, especially utility providers of gas and electricity.

You also have the peace of mind knowing that whatever payments are made are overseen by your bank, so it is a safe and secure environment. In the event that too much money has been debited from your account and you have been overcharged, you have the Direct Debit Guarantee scheme from your card holder that will be able to refund you.

One piece of advice is whilst you have your direct debits set up, it is always good to double check the amount going out each month. It is easy to sit back and watch the repayments going out but you need to be alert in case you are overcharged.

What is a Standing Order?

A standing order is similar to a direct debit in the way that you make recurring payments each week or month based on an amount you have set and date you have agreed with another party.

The only main difference is that you are setting up a fixed amount that you are paying each month e.g £500 rent per month. You are in control of this money and you determine the amount and the date that it is sent out.

Standing orders are perfect for rent, because you know that the amount charged will remain the same for several months or a year. If the rates went up and down each month, like utility bills, you would use a direct debit.

Another good use of standing orders is the ability to pay individual bank accounts whether it is sending money to another family member each month e.g £100 a month. Or in a smart way, you can send money to your own other savings account. Imagine that you want to put £300 aside each month for savings or a rainy day, well, you can set this up via your standing order.

Similar to a direct debit, you have the security of your bank or building society. They can be set up in your local bank branch, by post or most usually, the convenience of your own home by the phone or email.

Again, standing orders are free to set up. Since you have more control, it is your responsibility to double check that amounts that you are paying each month and make sure that you delete anything that you are not using as you could be getting charged. For any issues with your standing orders and the amounts being paid, simply contact your bank branch.

Do Loans Use Standing Orders or Direct Debits?

Most commonly, no. Loan companies, including guarantor lenders use a process called Continuous Payment Authority. This is a method of recurring payments whereby the lender verifies your account during the application stage and is then able to collect from your debit account only (not credit card) on a scheduled date.

The amount collected each month may vary month-on-month, so it is a bit more similar to a direct debit. In the same way, the lender has to give you notice before taking any repayments each month.

Whilst a direct debit allows you to cancel it at any point, you cannot ask the lender to cancel your continuous payment authority but you have the right to cancel by asking your bank directly. The only reason for cancelling would be to stop repaying your loan. Maybe because you have other payments elsewhere, but it is always important to communicate this to the lender so you avoid any additional fees.

The reason that lenders use CPA is because it gives them more flexibility to make repayments on a massive scale, especially if they have hundreds or thousands of repayments that are going through every month. However, lenders do incur a small fee every time they go to access your debit account for a repayment. They are limited to the number of times a day that they can access your account because ultimately the consumer should have the first choice and maybe they will need the funds for other purposes first like food or rent.