Finance Options to Improve a Property

Improving a property has many benefits; from being able to increase the property’s overall sell-on value or being able to get tenants on board and charge higher rents by offering better value.

For individual homeowners, a big living space, kitchen or loft conversion can offer a better quality of life and more living space for existing residents or family members to name just a few potential benefits.

What Can You Change?

Exterior

This makes your property look attractive from the outside, giving you a real kerb appeal and look snazzy from the curb of the road. This includes modernising the front door, windows, front garden and lighting to present a clean and attractive looking home.

Extensions

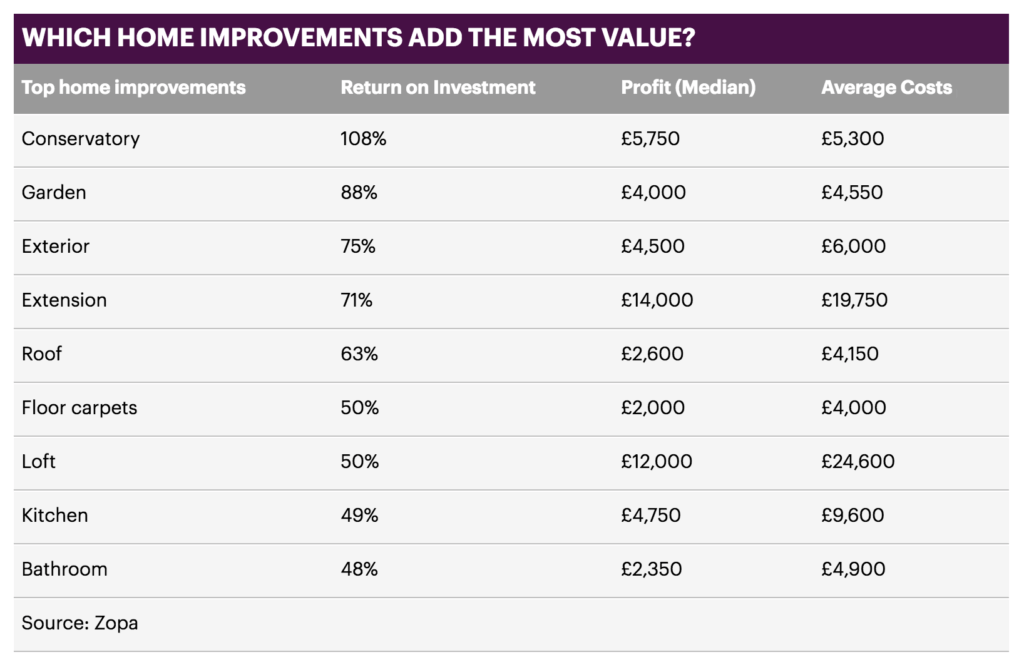

A loft conversion can add up to 20% to the value of your home and this can include a shower room and another room which can be used as a bedroom, playroom of home office.

A conservatory can add between 7% to 11% to the value of your property too and give you extra living space just off the kitchen (where we spend most of our time anyway).

For larger budgets, you can consider adding a basement which can offer huge spaces for you and your family – whether it is a gym, home cinema, office or similar. The cost of starts at around £300 per square foot (£200 for digging the land and £100 for the work you do on it). However, a well-constructed basement can add as much as 30% to the value of your home.

Interiors

Some basic home improvements include new carpeting, paint work, flooring and furniture. Adding a nice dining table, chairs and couches does not offer a great return on investment because this is something that you typically take away with you when you move house. But certainly an improvement to the floors, walls and carpets can help tidy up the feel of the house.

Other interior additions include a remodelling of a bathroom or kitchen and whilst this can provide a good return of around 5%, you have to cost it out effectively. This is because there is only so much that people can spend on a home and having a fancy kitchen worth over £100,000 on a road where the average home sells for £300,000 does not make sense.

Source: This is Money

Common Finance Options

For those who have the funds immediately available to improve a property of any sort, the process will be easy and will entail little more than comparing quotes and then instructing the relevant builder or project manager to commence their work according to the plans. Most property and homeowners will not necessarily have thousands or even tens of thousands of pounds available immediately, meaning they will need to borrow the money in another way.

What is important though is that the finance option that is best for the borrower’s needs, requirements and budget is the one used for the funding. There is no shortage of types of finance for properties either. Nowadays, lenders and brokers are available and they can secure all types of property finance such as that required for development, refurbishment and even entirely new builds (source: SPF Short Term Finance).

However, for smaller projects such as adding a new coat of paint and a new central heating system, both of which can increase the value of a property somewhat, it is far less likely that these formal property finance lenders will be willing to lend the money as they tend to focus on larger developments and projects. Therefore, it is worth exploring alternative and more likely loan options such as personal loans or family and friends.

Property Finance Lenders

These lenders provide the larger loans for property development and refurbishment and will also require the finance to be secured on a property to ensure they have ‘security’ on the loan. Loan amounts will range from £50,000 to £25 million. For example, a developer may have permission to convert a derelict warehouse into multiple housing units.

To do so, they may need to invest £250,000 or even more for the works required. It is likely that the property is worth significantly more than that and so if they have enough equity in it, they will qualify for the relevant development loan.

Once they have borrowed the money and have converted the property accordingly, they can then refinance the property, taking out a traditional mortgage to pay off the development loan and allow them to consolidate their debts and repay them over a manageable time frame. Alternatively, once the property is converted, they may simply sell it on at a profit, repaying the development loan whilst still making a profit.

Home Improvement Loans

These are specific loans for making renovations and refurbishments to your home. Applicants can borrow between £1,000 and £35,000 over one to five years and repay in monthly instalments or upon completion of the job.

Some home renovation loans come in the form of unsecured, meaning that they are not secured on your property or any other collateral. Your eligibility will usually depend on your credit history, income and affordability.

Some home improvement loans fall under secured, so you have to put down your home as security and risk losing this (or another valuable asset i.e a car) if you cannot keep up with repayments. However, since the lender has security and can recover their costs by re-sale of your asset, the interest rates can be very low at around 2-5% per annum.

Guarantor Finance

It may not be possible to secure development finance from a specialist lender for several potential reasons:

- The borrower may not own enough equity in a property to borrow against it

- The works to be carried out may be deemed ‘too minor’ (decorating or small improvements)

- The borrower’s credit rating may less than perfect

Guarantor loans however fill this void. Rather than having to go through a very long application process as would be required with banks and high street lenders and rather than risking the late payment charges of a payday loan, with a suitable guarantor (especially a homeowner), the borrower can secure their funds.

For example, a homeowner may be in the early stages of paying their mortgage and therefore does not have enough equity in the property to use it as security. . They may have a friend or family member who is unable to give them all the money they need, but who can guarantee the status of a loan of a few thousand pounds.

The homeowner can therefore apply for a guarantor loan with their friend available to ensure the loan is repaid should the borrower default.