Guarantor lending safer investment than peer to peer?

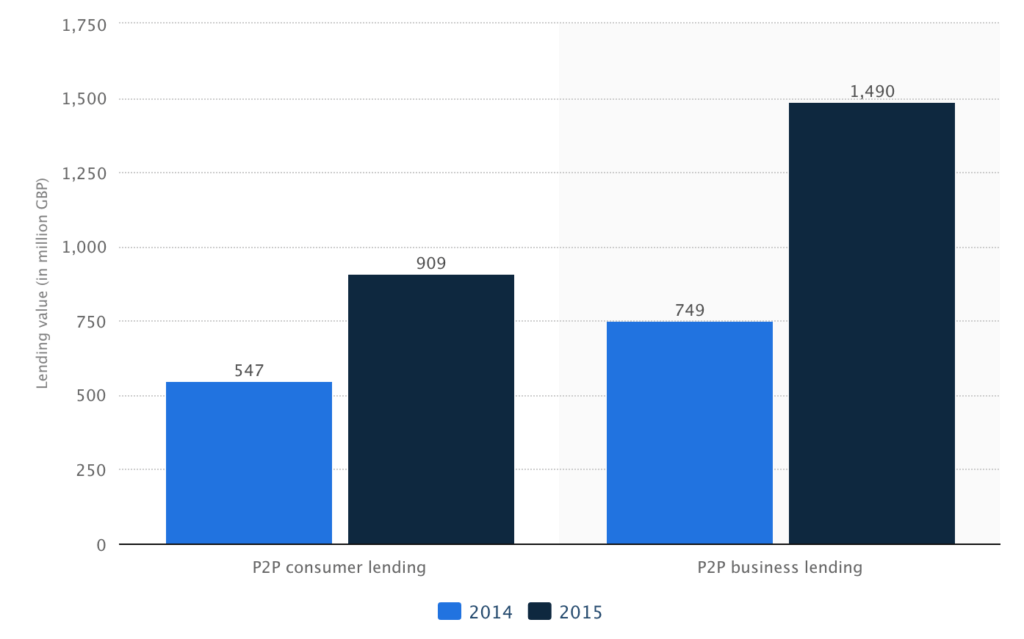

Peer to peer lending has grown significantly in the UK over the last few years. According to the Peer to Peer Finance Association, lending rose to £6.5 billion in 2016 in the UK, up from £2.1 billion in 2015.

The figures are based on customers borrowing up to £25,000 (Zopa) and £35,000 (Ratesetter) for personal loan use, business purposes or property finance (this could be secured). Interest rates range from 7% for good credit and up to 30% for bad credit (Source: MoneyAdviceService).

(Source: Statistica.com)

However, the money does not come from the lender itself, but it is funded by other people, known as ‘lenders’ – hence the name “peer to peer lending” or “p2p lending” for short. Lenders or investors get on board with the hope of receiving a better interest rate than they would at their local bank or savings account. This process turns an everyday person on the street into a potential lender and investor.

Lenders can choose their risk with good credit borrowers offering rates of around 3.5% and high risk borrowers offer a return of as much as 7% (Source: Moneywise). Investors can choose their risk and diversify accordingly. Companies state that you can lend as little as £10 and the maximum amount is unlimited.

Lenders or investors get on board with the hope of receiving a better interest rate than they would at their local bank or savings account.

The p2p lenders such as Zopa, Wellesley, Thincats, LendingWorks and more, will be responsible for transferring the loan funds and making collections too. They make money by taking a commission through the process or setting rates so that they can still take a slice of the action, known as ‘arbitrage.”

For the saver, although your money is at risk and you could end up saving nothing, this is very unlikely and the calculated risk means that more than 90% of the time, you will get the interest rate promised. Your money is not covered by the Financial Services Compensation Scheme so unlike a credit card, if you lose money or the company goes bankrupt, you cannot claim it back.

Depending on the lender, you may not be able to exit within a period of time e.g 1 year and your investment may also be locked away and you cannot access it. Please read the terms and conditions of the lender. Usually, the more you lock it away and less access you have to it, the higher the returns will be.

Could guarantor products offer better returns?

The answer is yes, very possibly. Since peer to peer finance is based on unsecured loans, there is always the risk the lender will lose their money that they lend out. However, it is clear that guarantor loans have a much lower default rate because there are two borrowers involved and for the very least, if the main customer fails to meet repayment, they have a guarantor with a good credit rating to back up the loan.

One company that has acknowledged this is Emoneyunion who seem to be the only p2p lender that are offering savings rates based on guarantor loans. The rates are as high as 10% for successful lenders, which is higher than the 7% or 8% proposed by other peer to peer lenders. The reason for the higher savings rate on offer is firstly because the default rate is lower, so there is less risk involved. Secondly, the rates for guarantor loans are higher than your average peer to peer loan, with rates ranging from 39.9% to 59.9% representative APR.

Initially, the loans are offered as unsecured provided that you have the credit history to back this up, strong income and affordability. If not, you have the option as a borrower to add a guarantor to your application to secure the funds you need – and this extends so lenders can invest with them too.

How Peer to Peer compares to other types of finance

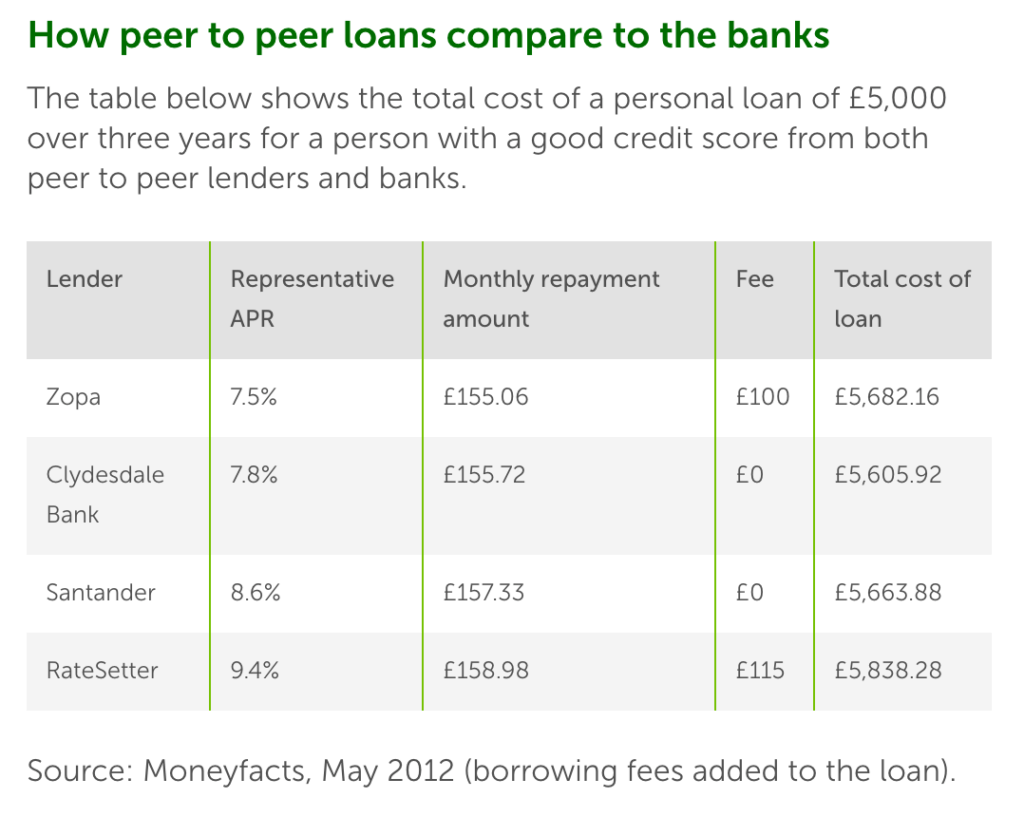

The rates charged for personal loans are very similar to high street banks, except there is fee involved usually of around £100.

For borrowing, there are cheaper alternatives available such as borrowing from family and friends which is usually free. One can also apply with their local credit union which comes to 1% per month and no late fees if you default. It is because they are non-profit organisations or set up by a group of people with a common goal e.g local church or community centre.

For savings, as mentioned, the rates are far better than a typical ISA or savings account from your bank which may only provide 0.5% to 1.5% so finding alternatives like this can be very appealing indeed. Other similar alternative investments include real estate investing, momentum investing and crowdfunding.