How to get lenders to stop calling you

If you are experiencing difficulties with making repayments for a guarantor loan, payday loan or with a credit card, you are most likely to receive phone calls, letters or emails from your creditor or third party debt collectors contacting you in order to sort out getting back on track with your repayments.

Whilst this is a normal step for lenders to take, as part of the process of what happens when customers default on their loan, you may find that it makes you feel more stressed about the debt that you are in, which can contribute to a feeling of being overwhelmed, which may not necessarily be conducive when it comes to trying to get your finances sorted. However, there are ways in which you can deal with the issue of stopping lenders calling you. We take a look at how you can tackle this in a positive manner.

Contact your lenders

Whether you have one loan outstanding, or multiple, your very first step to dealing with lenders contacting you by phone is to contact them yourself. In a situation where you are experiencing debt, the very last thing you should do is be an ostrich with your head in the sand, avoiding any contact with creditors because you are stressed out about being behind with repayments. Whilst not the easiest of things to do, you will feel much better for contacting them. By explaining your situation to the creditors, it can help you to go forward, and prevent potentially endless phone calls too.

Freezing interest

One of the advantages of contacting your creditors as soon as possible when you are experiencing financial difficulty is that they may agree to freeze interest on your outstanding loan.

This is particularly important, given that certain types of loans can accrue interest of up to 0.8% a day (a price cap has been implemented by the Financial Conduct Authority since they took over from the Office of Fair Trading in 2014), which if you are having problems with money, can make the process of getting back on track harder. However, by contacting your lenders directly, they could offer freezing interest for a period of time (or potentially completely) so that you can find it easier to start paying back.

Set up a payment plan

Another reason that it is important to get in contact with your lenders is so that you have the opportunity to arrange a more feasible payment plan.

Perhaps your financial circumstances have unexpectedly changed since you first took out the loan in question, and now it means that you have less income per month than you previously did, meaning that you can’t keep up with the same repayment plan that you had before. If you explain the situation to a creditor, they may agree to a new payment plan (though you should be aware this may accrue additional interest if it means that the new payment plan is spread out over a longer period of time) which is more manageable, and prevents you from receiving phone calls from creditors.

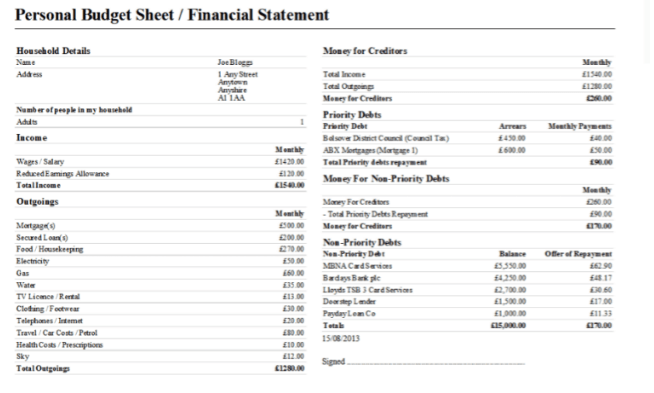

Enter debt management

If you are finding it very difficult or too overwhelming in order to be able to get in contact with creditors (that may be especially the case if you have a number of different debts outstanding) you could consider consulting the support from a debt management company.

Otherwise known as debt relief or debt consolidation, these companies help to create a payment plan as well as an agreement that helps to you to pay the outstanding debt without leading you into further financial difficulties. These companies can take away the stress and fear of contacting lenders yourself as they can do this on your behalf, making it less time-consuming for you too. Generally speaking though, debt management services are most suited to those in one of the following circumstances:

- If you have County Court Judgements against you

- If you are experiencing bankruptcy

- If you have a number of credit card, secured loans and payday loans outstanding

Furthermore, there is only certain kind of debts (known as non-priority debts) that can be included in a debt management agreement. Those considered as ‘priority debts’ such as council tax, income tax, rent or mortgage arrears have to be dealt with separately, and before consulting the services of debt management services. Non-priority debts can include the following:

- Water charges

- Store card payments

- Benefit overpayments

- Bank loans

- Credit cards

- Student loans

What about if I’m being harassed by a lender?

Most lenders will only contact you a suitable number of times in order to settle a debt, and will behaviour in a fair way to the consumer. For example, the creditor has the right to take reasonable steps to retrieve the money back (e.g. send demands and reminders for payment, telephoning you for payment, taking court action). However, a small minority of creditors do not act in this way when trying to recover their money.

What counts as harassment?

- Threatens you verbally or physically

- Puts pressure on you to pay all the debt off when it is simply not possible for you to afford it

- Pursues you on social networking sites

- Makes false claims to be a bailiff or work for the court

- Implying that is possible for legal action to be taken when it can’t

- Not letting you know if the debt has been passed on to a debt collection agency

What can I do?

Your first step should be to complain directly to the creditor, but if this does not work, you can contact a professional body, such as the Standards of Lending Practice.