How Loan Companies Do Underwriting

What is Underwriting?

Underwriting refers to the process taken by a lender or finance provider when they review an application and make a final decision on whether the applicant is approved for a loan. The individual or team of people carrying out the process are known as ‘underwriters’ and they will make their decision based on a series of checks, behaviour and statistical analysis to approve those customers that are best suited to their product and most likely to meet repayments.

Disclaimer: All lenders have their own criteria based on the products they offer and their own fee structure and procedures. This is an overview of the practices used by lenders in the UK and is not specifically for one lender or all lenders, it is purely a guideline.

The entire underwriting procedure involves a combination of automatic and manual processes so that a lender can receive several transactions per day and narrow it down to their best applicants. The loan acceptance process is commonly referred to as a funnel whereby the most applications come in at the beginning and all the different checks whittle it down until the small end of the funnel where only a minority are successfully funded.

How Long Does a Loan Stay in Underwriting?

A loan will typically stay in underwriting for a few hours before a decision is made by the lender or however long it takes to carry out the further checks and make a decision.

A loan can be in underwriting for longer if the application is over a weekend or holiday or if the lender is waiting on information from the applicant such as a payslip or bank statement. Once it gets to 30 days, the applicant will probably need to re-apply and things like credit checks and affordability checks will need to be run again to get an up-to-date version of the loan application.

Initial Application

All lenders start with an initial application whether it is for a loan or credit card. Applicants are asked to fill in their details on paper or online and this usually only takes a few minutes. The idea is that these fields are supposed to tell the lender who meets the basic criteria of the loan by asking for things including:

- Age

- Employment Status

- Monthly Income

- Homeowner vs Tenant

- On Benefits

- Bank Details

All lenders have a set criteria for the ages they are allowed to lend to (usually 18 years) and some providers will require applicants to be employed and living on a minimum income each month. Therefore, this basic form allows the information to be automatically processed by the lenders and if the individual does not meet the basic criteria, they will be declined straight away.

But if they meet the initial criteria, they will be passed onto the next stage. Usually this requires the main borrower (and their guarantor) to sign a loan agreement highlighting the terms of their loan including repayment dates, amounts owed and what is required of them. The loan agreement can be printed off, signed and posted back to the lender but to make things quicker, the majority of online customers opt for ‘electronically signing’ the document, whereby they verify the paperwork using an email link and PIN code sent to their mobile phone. For more information, see how a guarantor loan application works.

Initial Checks

In the next stage, the loan provider or broker will have people that are eligible for a loan but now need to determine whether they are who they say they are and if they have a worth credit score and the affordability to pay their loan on time.

The following processes are usually automated and use credit technology. This is so lenders can proceed with the applicants that meet their criteria and remove any ones that do not. For a loan company to be scalable, they need to be able to process several hundred or even thousands of applications per day, so they are eager to automate effectively and verify the best customers.

Personal details checks: The automated checks should be able to tell whether the person applying is really that person. This includes using address-matching technology and also matching their bank details with the individual. If this information does not match, it will raise a flag on the lenders system.

If the flag is deemed serious, like completely different address and bank details, this might raise a red flag. Lenders can choose how many red flags they are willing to allow in order to pass the customer onto the next stage of underwriting. Perhaps one red flag is enough to be declined, it depends on the lender’s criteria.

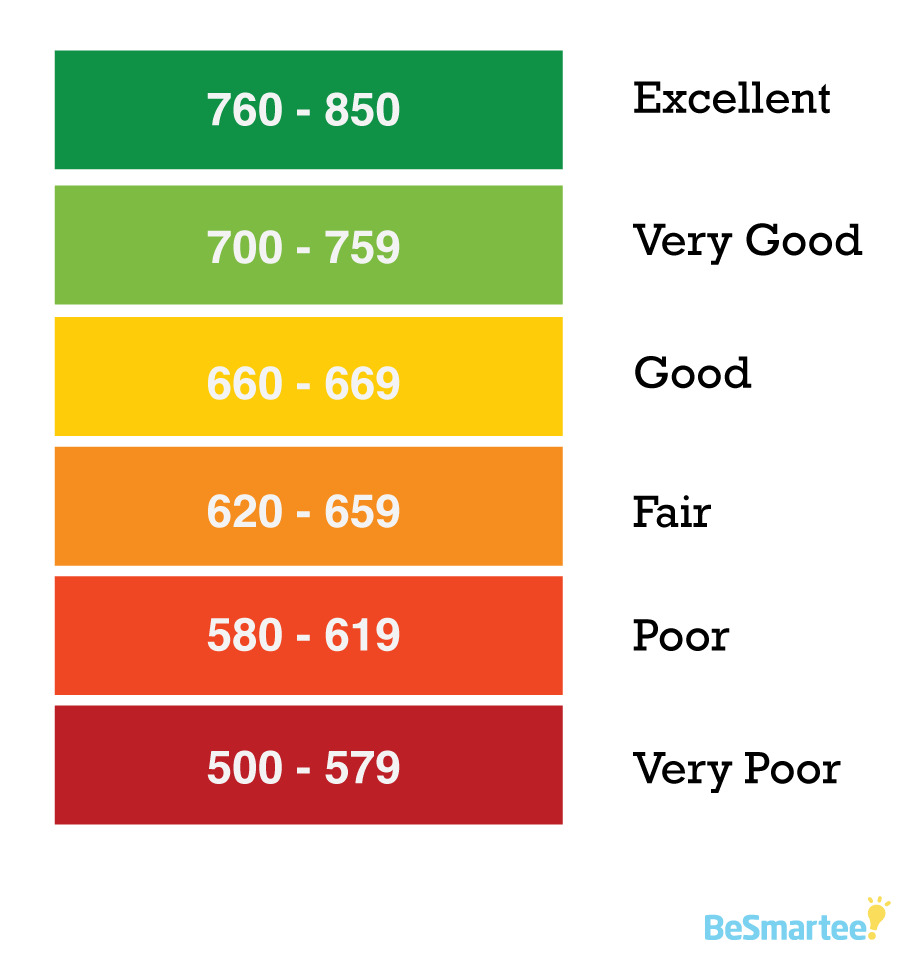

Credit Checks: One of the most fundamental parts of deciding who gets a loan is whether they have passed the relevant credit checks. If having a strong credit score is part of the criteria, the lender will typically work with a credit reference agency like CallCredit or Experian and pay a small fee for accessing the credit information of each customer, usually done in an instant.

The lender can set a certain credit score to be eligible for the next stage e.g must be over 650 or will accept over 500 if other signs are good. This is crucial to lending effectively, as the lender can change this score regularly based on their lending appetite. So if they want to lend more and accept more risk, they can lower this score or up it if they want to be more strict.

For payday loans, only the individual’s credit score is important. For guarantor lending, the main borrower’s credit rating may be less significant but instead having a guarantor with a strong credit score is crucial to back up the loan and repay on the main borrower’s behalf if they do not keep up with repayments. For more information, read our guide on the checks carried out by guarantor lenders.

Manual Underwriting

The manual part of underwriting requires a human to physically action a task. During the loan application process, this typically involves a member of the team like the customer services agent to call the applicant and confirm some details over the phone. For a guarantor loan, it involves making sure both the borrower and guarantor under their role and what is required of them during the loan term.

During this stage, lenders may ask request additional documents to confirm various details of income, employment and bank details. Therefore, they may request a pay-slip, p45 or bank statement to cross-check their details. This customer agent will receive this information usually by post (rarely by post as it takes longer) and check the documents. Once they have this information, the advisor can decline the customer, request further information or pass them onto the next stage of the process.

Decision

This is the final stage of the underwriting procedure and usually involves a more senior level staff to professional underwrite the application. Here, the team member will review all the information they have received thus far about the customer (and their guarantor).

The underwriter will have access to information on a senior level so they will know what type of customer they want to approve, how much they can lend out and the amount of risk that they can take on. The main underwriter will also consider various behavioural and historic factors when making their decision. This includes understanding the default rate at a top level and using things like time of the month, age, profession, residential status and gender when concluding to fund the person or not.

One of the most key checks is ‘affordability’ which aims to match how much the customer wants to borrow with what they can afford to repay without falling into debt. A good underwriter is able to adjust the amount the person wants to borrow so that they can make affordable repayments and not go into default. So the underwriter will consider the applicant’s monthly income (which should have been confirmed), their monthly expenses and how much they have asked to borrowed when making their decision.

Funding

Provided that the customer and their guarantor have confirmed all their details, have a strong credit score and affordability, their application can be sent to funding. Most online lenders fund to a BACS account so the money is transferred within 48 hours to the individual’s debit account. Although, if it is a guarantor product, the money will be sent to the guarantor so they have a cooling period for two weeks and they can pass on the funds to the main borrower or send the money back to the lender without a charge.

To reduce fraud, funding must usually go through at least two people working in the organisation. This avoids a member of staff funding loans like no tomorrow without authorisation.