Google to stop showing paid adverts for payday loans and guarantor loans

Last week, Google made a huge announcement that they will not longer be allowing payday lenders to advertise in the paid section of their search results. This has huge implications for the £2 billion payday loan industry in the UK (and of course the US where the policy is originated).

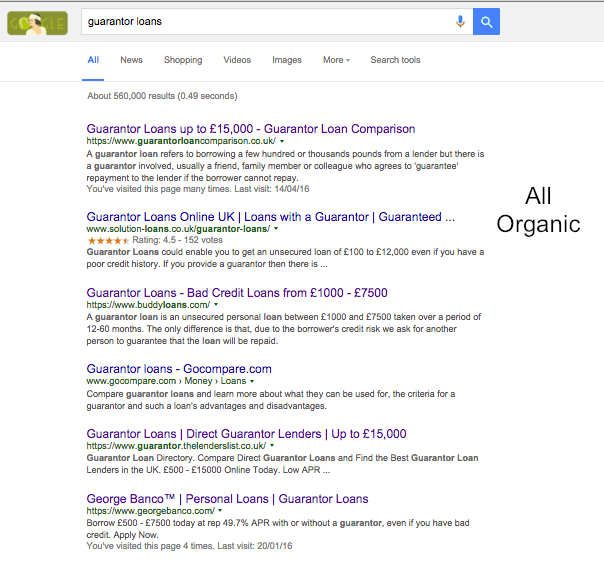

How the search results could look

Provided that the new policy bans all adverts for guarantor loans, the search results will go from looking like this:

To this:

As you can see, the removal of paid adverts will give a lot more exposure to the organic search results. Currently 4 of the 6 results you can see are paid adverts so you are far more likely to click on them (and generate revenue for Google) but this could potentially change when the new policy comes into effect.

Why did Google make this update?

The new policy update which will go into effect on 13th July 2016 on Google and has already been implemented by Bing was introduced as Google ‘have reviewed their policies and show that these types of loans can result in unaffordable payment and high default rates for users’ and so it is something that they want to stay away from.

Google: When reviewing our policies, research has shown that these loans can result in unaffordable payment and high default rates for users so we will be updating our policies globally to reflect that.

Payday loans will therefore be joining other no-go products that are banned from paid adverts on Google including firearms, recreational drugs, tobacco and adult themed media.

The laws of the new policy state that no paid adverts will be shown for payday loan related products or anything with an APR that is higher than 36% or where payment is due within 60 days. Since the average payday loan has an APR of 1,270% (Mr Lender) and lasts up to 45 days, it certainly falls within this category.

This rule of no APR higher than 36% originates from a price cap introduced in the US for the National Consumer Law Center and their paper here, argues why the 36% is such a crucial figure.

So whilst payday products will be banned from Google’s PPC adverts, this update will not affect will not affect companies offering loans such as Mortgages, Car Loans, Student Loans, Commercial loans, Revolving Lines of Credit (e.g. Credit Cards).

What is still yet to be decided

What has not been fully confirmed is whether this new policy will impact the guarantor loans and logbook loans industry in the UK. With guarantor loan products ranging from 39.9%-49.9% APR and logbook loans from 100% to 300% APR, they are certainly above the 36%, but this has only been mentioned for US products, so no full confirmation for the UK just yet. Although when I asked this under the comment section, some dude said ‘yes it will’ which is compelling but still not verified.

Another consideration is whether there will be no paid adverts at all or just no paid adverts from payday lenders. For instance, could debt management companies or charities advertise to people searching for payday loans? Or could companies that offer low cost alternatives perhaps advertise there too e.g credit unions

An article in TechCrunch originally said other companies would be able to advertise but after I questioned this in the comments, they changed their statement to saying there will be no paid adverts at all and just organic search results.

A final question is how Google can so tough on the payday loan markets in the US and UK when it invested $14m in a company called Lendup which offers payday loans with a 600% APR thatare repaid over 45 days? The irony is that they will still have to ban their adverts.

However, LendUp has a slightly different proposition and is geared towards helping US consumers overcome payday loans. For instance, when a customer repays a loan on time, it significantly boost their credit score (more so than in the UK) and they can work their way up a repayment ladder to get the best credit score possible.

Then on their next loan, they can borrow more at lower rates, which seems contradictory to most payday lenders but allows people to get out of the debt spiral. Finally, if they repay a certain number of loans on time, they will have access to a zero percent interest credit card which they would probably never get from somewhere else given their credit history. So there is huge emphasis on improving peoples’ credit scores and getting them out of the payday cycle.

The implications of Google’s ban on payday loan related products

This new policy will have huge implications on the payday loan sector in the UK which has already been faced with a lot of recent challenges including a price cap of 0.8% introduced by the FCA in January 2015, the 12-month process to get FCA authorisation and stricter criteria which resulted in payday giant Wonga reporting annual losses of £80 million.

More competition for organic search results

Naturally, with paid adverts being removed, the competition for the natural search results or SEO will become highly competitive. For some companies spending tens of thousands of hundreds of thousands on PPC per month, this could all be shifted into their SEO.

Whilst Google has dabbled with a payday loans algorithm before, we could see a new organic search algorithm for high cost loans – so instead of just lenders, you will also see news and charities to get a full picture of the industry.

Barriers to entry

New firms that enter the market won’t be able to get instant traffic by throwing money into paid advertising. They will have to wait a minimum of 6 months for their organic search rankings to manifest. This reduces competition in the industry and the online loans sector will be seen less of a quick rich opportunity.

Lower profits for stakeholders

For various companies that generate huge returns from PPC, they will likely see lower profits and have to invest elsewhere to generate a similar return e.g through TV, radio, email or repeat business.

We know that this policy will definitely go ahead for payday loans but whether it will impact guarantor loans too, we will have to see this July!