Why didn’t I get the interest rate advertised for my loan?

Every year, borrowers are left scratching their heads as to why they may not have received the rate advertised. After all, if I have a strong credit score, good employment and homeowner status, surely this should give me the lowest rates? For many consumers it comes as a real surprise when they receive their ‘SECCI’ or loan agreement and see that it is not the rate on the website or brochure.

In an article by This is Money, they tell the story of a company director with a 999 credit score who applied for a Halifax credit card and was offered 21.9% against the 12.9% advertised rate. Another case study shows a 54 year-old woman with a perfect credit score who received a 12.9% rate for a £20,000 advertised at 6,7%.

The question begs: If the Representative APR for a guarantor loan ranges from 39.9% to 49.9% depending on the lender, then why am I getting rates like 43.7% and 52.3%?

Logically speaking, lenders should be rewarding the best credit scores with the best rates. The stronger the customer’s credit and affordability profile, the more likely they are going to receive their repayments on time – so having less risk should lead to a lower interest charged. It can also act as an incentive to those with bad credit scores – as improving your credit score to get access to the best rates is very appealing.

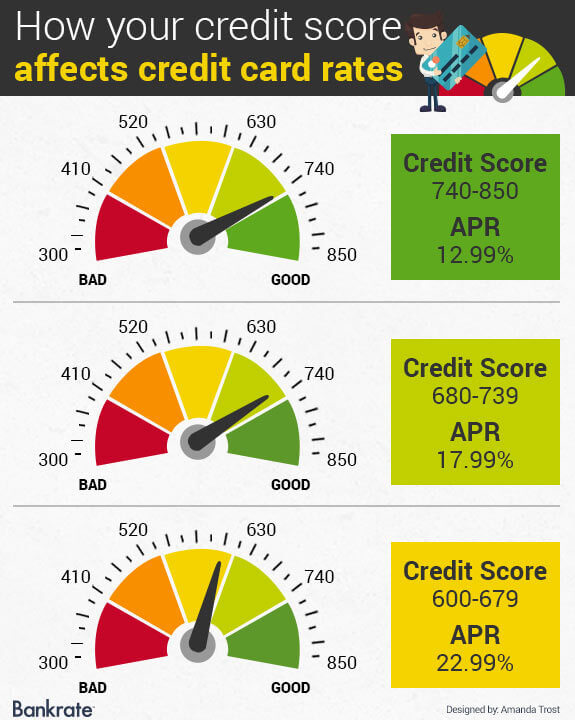

This is how credit cards work – whereby you pay lower rates based on your credit score and some peer to peer lenders operate in this way too when you look to borrow money. Bad credit borrowers have a higher risk of default, so you typically see higher interest rates on loans and particularly credit cards. Read here more about how your credit score affects your cost of borrowing.

So why do I not get the rate advertised????

Understanding the Representative APR

Not many people know that the representative APR advertised is only available to 51% of successful applicants, as per The Consumer Credit EU Directive. This ruling is a fair and logical approach because it implies that lenders must be giving the advertised rate to slightly more than half the borrowers they fund. It also means that lenders have no obligation to give you anywhere near the representative APR if you fall into the other 49% – so you could pay far more if they decide to.

You may also see the ‘typical APR’ and this is the rate that must be provided to at least 66% of successful customers. The factors that might affect the rate you get include your credit score, the length of your loan and obviously the lender that you work with. There are some cases where an APR can seem very high (e.g payday loans) and this is because although they are expensive, they are only meant to last a couple of weeks and to be expressed as an APR they are compounded multiple times – making them seem higher.

Affordability Checks

Lenders explain that you may not get the rate advertised due to additional affordability checks. This is where they look very carefully at the ratio between your income and debt to see how much you can afford. To calculate this, they may request your monthly expenses on rent/mortgage, food, credit cards and ask for proof of these with a bank statement.

If the lender determines that you have other liabilities such as credit card bills, mortgage payments or several dependents, it is understandable that they may not give you the lowest possible -because you have other financial commitments and still present some kind of risk. So in the case of the company director with a perfect credit score, the lender cannot deny other financial commitments.

Loyal Customers Are Rewarded

The article from This is Money explains that loyal customers tend to have access to better rates. Perhaps this is a borrower taking out a second, third or fourth personal loan from the lender and has developed a good track record, whilst their credit score and affordability has maintained strong.

For banks, they may offer preferential rates to customers who have accounts with that specific company and show a healthy use of transactions. For instance, Barclays are more inclined to give their own account holders better rates than someone who banks with a competitor like Natwest or Santander. Loyalty will get you far – but you will take you time to get the lowest rates.

Newsflash: You Can Ask The Lender Why

For some clarity on the issue, you are allowed to ask the lender why your application was rejected or you were given a lower rate than anticipated. They will not tell you this straight away or out in the open, but as part of the EU Directive, you are allowed to request this information and they will formally write to you. So all is not lost, you can receive some closure.