Understanding the costs of guarantor loans

As a comparison site and part of our commitment to responsible lending, it is important that we explain the costs of a guarantor loan and how to measure and understand them effectively. With a number of loan products available, it can be hard to know which one is the best and whether you are getting a good deal. So we look at the following factors which give a further insight into understanding the costs of guarantor loans.

- The APR

- Representative Example

- Loan duration

- Repaying early

- Cashback

Understanding the APR

The APR is probably the easiest way to compare the cost of a loan or any financial product. This measurement is enforced by regulators of all financial products as a means of comparing different cards, loans, savings accounts and more.

In this particular industry, lenders are required to clearly state the Representative APR on all marketing information and contractual agreements. So it is common to see the representative APR for each lender on our website and on their own websites too.

APR stands for the ‘Annual Percentage Rate’ and represents what the loan would cost as though it was taken out for an entire year. Whilst most lenders we feature charge 49.9%, there are some cheaper loans available but be sure to check the terms such as loan duration and amount you can borrow.

The calculation for APR can sometimes be very complex but the easiest thing to do is take the interest/loan amount x 100.

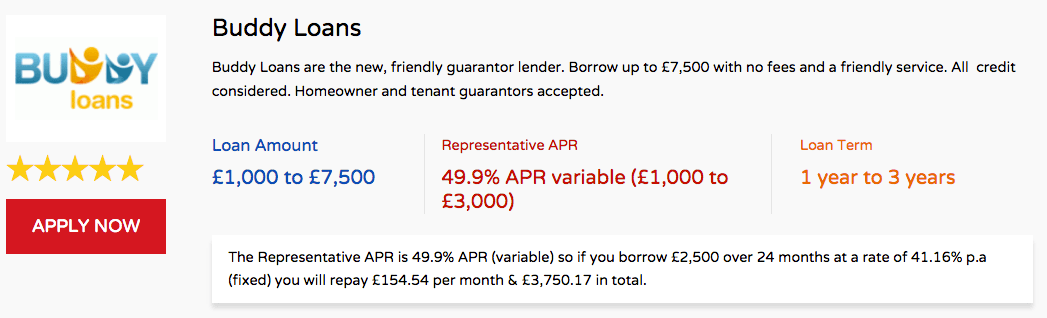

Here is an example from Buddy loans:

If you borrow a £2,500 loan over 24 months and the interest is £1,250, so the total is £3,750 to repay

£1,250/£2,500*100 = 49.9%

For more information, read our guide on APR and why it is used.

Paying the interest

Your loan is made up of interest and capital. The capital is the amount you borrow e.g £1,000 or £2,000 and the interest is the rates charged by the lenders which they choose.

So when you are repaying your loan, each month you start by paying off most of the interest first and a little of the capital but this switches by the end of the loan term.

Very similar to a mortgage, you can see the capital increasing over the time and the interest decreasing over time.

Look at the Representative Example

The calculation above is a good representative example. It gives a full breakdown of what you are borrowing and what you will repay. So whilst these may not be the exact loan terms you are looking for, it does give you a good example of what you could be paying.

The term ‘representative’ means that this is the rate that at least 51% of successful customers will receive. So you know that if you apply and your application is successful, this is more of less what you should receive. The rate will depend on how long you have the loan open for an how much you borrow. But of course, every lender will have their own rate which they provide.

Check the Loan Duration

The loan duration is important, with lenders generally offering loans for 12 months to 60 months (equivalent of 1 to 5 years).

Typically the shorter the loan, the higher the APR will be because it gets multiplied until it is shown as an annual figure. So you must consider the length of the loan when you get the representative example.

In most cases, the longer the loan, the easier it will be repay as you are spreading repayments over a longer period of time and only making small repayments every month.

How does repaying early affect the amount you pay?

Repaying your loan early will significantly change the cost of your guarantor loan. It is very common to repay a loan like this early because they are typically used for emergency expenses like paying for a broker boiler or a funeral. So you may not necessarily need a guarantor loan for as long as 5 years and if you have the income to pay it off early, then why not?

All the lenders we feature will allow you to repay your loan early and its cheaper to do so because you won’t be accumulating interest and you’ll only be charged the amount of time that you have had the loan open for.

Can I get cashback?

We happen to work with one lender in particular called Guarantor My Loan who offer cashback on your last monthly repayment. The way cashback works is that they put the money into your bank account, hence you get the cash,back.

This is their way of rewarding you for making all your payments for your loan and it encourages you to make them too, because it makes the loan cheaper in the end.

Our Values

At GLC, we believe that it is important for applicants to know exactly what they are getting when they apply and that they shouldn’t receive any surprises.

This is why we are passionate about constantly updating our blog and making sure that consumers have the right information to make an informed decision on their loans.

Our site is free to use and always will be. We simply take a commission from the lenders if an application is successful. We will never request any data from our customers and therefore we will not sell them on to any other companies.